A vehicle for Predictable, Safe, Tax-Efficient Wealth for Lifetime: Protection from Market Downturns, Tax Advantages, Flexibility, and Growth Potential.

An Indexed Universal Life Insurance (IUL) policy is a type of permanent life insurance that offers both death benefit protection and the potential for cash value growth linked to stock market indexes like the S&P 500. This cash value growth is tax-deferred, and IULs provide a way to participate in market gains without the risk of losing money when the market declines.

Features and Benefits

Accessing Tax-Free Income

You can access the cash value in an IUL through tax-free withdrawals or policy loans. These funds can be used to supplement retirement income or meet other financial needs without triggering taxable events.

Flexible Premiums

Customizable options to adjust premium payments, payment frequency, and death benefit amount.

Tax Benefits

IULs offer significant tax advantages, including tax-deferred growth, tax-free withdrawals up to the amount of your contributions, and a tax-exempt death benefit. These benefits make IULs an attractive option for those seeking to minimize taxes during retirement.

Permanent Coverage

Ensure timely premium payments to maintain lifetime coverage. Get lifelong protection for yourself and your loved ones in various situations.

Safe & Growth

Never risk losing your principal while enjoying steady growth within a set range each year, typically capped at 9% and floored at 0%, based on index returns like the S&P 500. This offers greater cash value potential than traditional fixed-interest universal life insurance and guarantees no less than 0% return, even if the market drops.

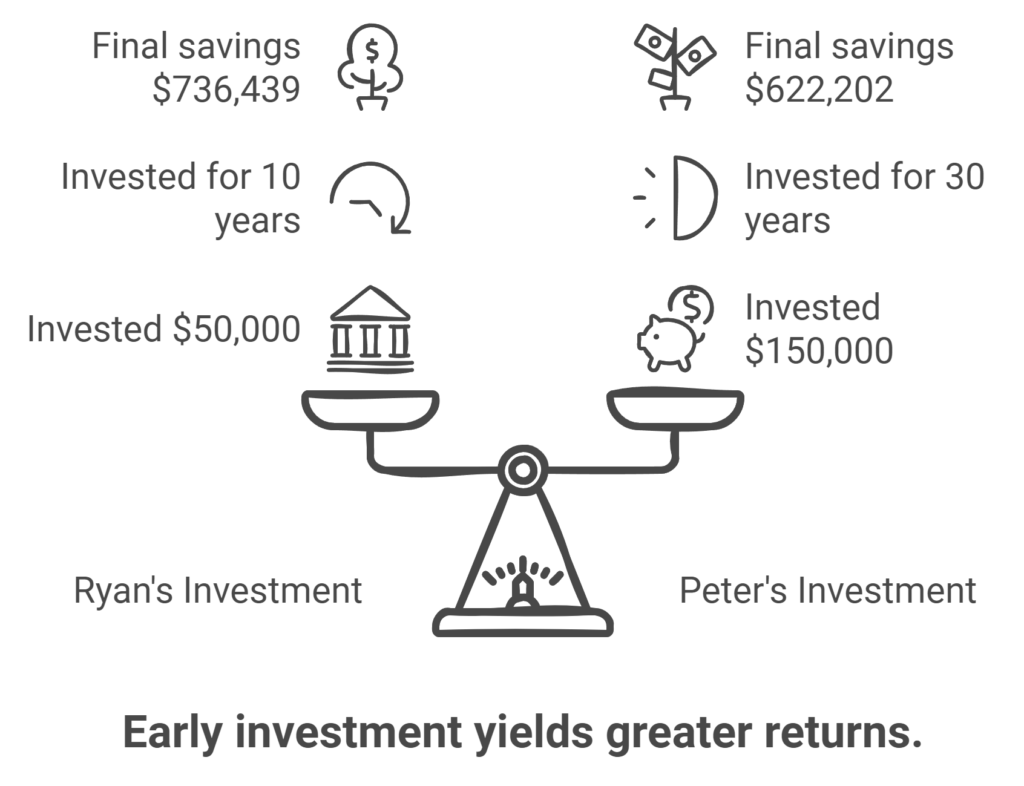

The Power Of Starting Earlier

Ryan: $736,439 at age 65

Paul: $622,202 at age 65

Consider how 25-year-old Ryan decided to invest for just 10 years, putting in a total of $50,000. After that, Ryan stopped adding any more money. Even so, Ryan ended up with more savings than Peter, who invested for 30 years and contributed three times as much, totaling $150,000.

This example highlights the power of starting early. The earlier you begin saving, the more your money can grow over time, thanks to the incredible effect of compound interest. As Einstein famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” So, start saving now and make each year work for you!

*Please note that tables and charts are meant for illustration only and do not represent any specific insurance policy. For precise details, refer to your individual policy. All guarantees and obligations depend entirely on the issuing life insurance company’s ability to pay claims. The example assumes an annual interest rate of 6.44%, with approximate values shown.

To provide you with the information you need quickly and easily.

What is Indexed Universal Life Insurance?

Indexed Universal Life insurance is a type of permanent life insurance that offers flexibility in premium payments and potential cash value growth linked to stock market indexes, like the S&P 500.

How does Indexed Universal Life insurance work?

IUL policies allow policyholders to allocate premiums into a fixed account and an indexed account tied to market performance. The cash value growth is based on the performance of the chosen index, with downside protection against market losses.

Is Indexed Universal Life Insurance a good investment?

Indexed Universal Life Insurance can be a flexible tool for those seeking life insurance coverage combined with potential cash value growth. However, it's essential to understand the risks and benefits compared to other investment and insurance options.

What are the benefits of Indexed Universal Life insurance?

Benefits include potential for cash value growth based on market indexes, tax-deferred growth of cash value, flexibility to adjust premiums and death benefits, and options for policy loans or withdrawals.

Can you lose money in Indexed Universal Life insurance?

While IUL policies offer downside protection against market losses, returns may be limited during market downturns due to caps or participation rates set by the insurance company.

How do I choose the right Indexed Universal Life insurance policy?

Choosing the right IUL policy involves considering factors such as your financial goals, risk tolerance, understanding of policy features, and comparing offerings from different insurance companies.

More Questions? We have answers.

Life insurance can be complicated. Luckily, we’re always here to help.